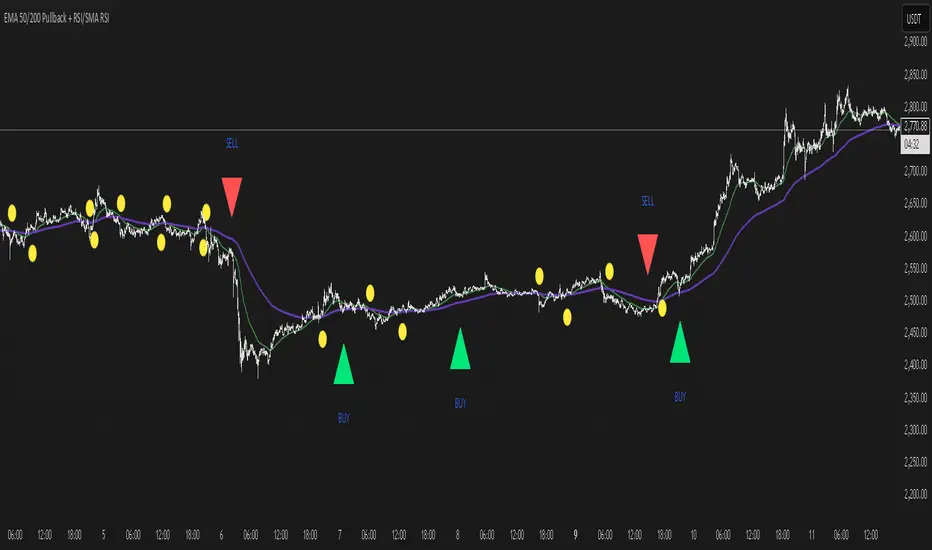

EMA 50/200 Pullback + RSI/SMA RSI

Strategy Description: EMA 50/200 Pullback + RSI/SMA RSI

1. Trend Identification with EMA:

Uses two Exponential Moving Averages (EMA): a fast EMA (default 50) and a slow EMA (default 200).

When the fast EMA crosses above the slow EMA (bullish crossover), an uptrend is identified.

When the fast EMA crosses below the slow EMA (bearish crossover), a downtrend is identified.

The lengths of both EMAs are fully customizable.

2. EMA Distance Condition:

Signals are only valid when the absolute percentage distance between the two EMAs is within a user-defined range (default: 0.4% to 1%).

This helps filter out weak signals when the EMAs are too close or too far apart.

3. Pullback Condition:

After a new trend is detected (EMA crossover), the strategy waits for the price to pull back to touch or cross the fast EMA (EMA 50).

This ensures entries are not taken immediately at the crossover, but after a retracement to a dynamic support/resistance area.

4. RSI Confirmation:

Uses the RSI indicator (default 14) and its Simple Moving Average (SMA RSI, default 14).

Buy signal: RSI crosses above its SMA.

Sell signal: RSI crosses below its SMA.

Both RSI and SMA RSI lengths are fully customizable.

5. Entry Rules:

The indicator only gives the first buy/sell signal after each EMA crossover (start of a new trend), and will not repeat signals until the next EMA crossover.

Buy signal:

Fast EMA crosses above slow EMA

EMA distance is within the valid range

Price pulls back to the fast EMA

RSI crosses above its SMA

Sell signal:

Fast EMA crosses below slow EMA

EMA distance is within the valid range

Price pulls back to the fast EMA

RSI crosses below its SMA

6. Customization:

All parameters (EMA lengths, RSI length, SMA RSI length, EMA distance range) can be adjusted in the indicator’s settings.

Note:

This is a signal indicator, not a complete trading strategy. For real trading, always combine with risk management and additional confirmations.

在腳本中搜尋"the strat"

Zero Lag MACD + Kijun-sen + EOM StrategyThis strategy offers a robust approach to identifying high-probability trading opportunities in the fast-paced cryptocurrency markets, particularly on lower timeframes (e.g., 5-minute). It leverages the synergistic power of three distinct indicators to confirm entries, ensuring a disciplined approach to risk management.

Key Components:

Zero Lag MACD Enhanced Version 1.2: This core momentum indicator is used to identify precise shifts in trend and momentum, offering reduced lag compared to traditional MACD. Entry signals are filtered based on the histogram's position (below for buys, above for sells) to enhance signal reliability.

Kijun-sen (Ichimoku Cloud): Acting as a dynamic support/resistance and trend filter, the Kijun-sen line confirms the prevailing market direction. Long entries are confirmed when price is above Kijun-sen, and short entries when price is below.

Ease of Movement (EoM): This volume-based oscillator provides crucial confirmation of price movements by measuring the ease with which price changes. Positive EoM confirms buying pressure, while negative confirms selling pressure, adding an essential layer of validation to trade setups.

How it Works:

The strategy generates entry signals only when all three indicators align simultaneously:

For Long Entries: A Zero Lag MACD buy signal (crossover below histogram) must coincide with price trading above the Kijun-sen, and the Ease of Movement indicator being above its zero line.

For Short Entries: A Zero Lag MACD sell signal (crossover above histogram) must coincide with price trading below the Kijun-sen, and the Ease of Movement indicator being below its zero line.

Entries are executed at the open of the candle immediately following the signal confirmation.

Risk Management:

Disciplined risk management is paramount to this strategy:

Dynamic Stop-Loss: An Average True Range (ATR) based stop-loss is implemented, set at 2.5 times the current ATR. This adapts the stop-loss distance to market volatility, ensuring sensible risk sizing.

Fixed Take-Profit: A consistent Risk-to-Reward (R:R) ratio of 1:1.2 is applied for all trades, promoting stable profit realization.

Customization & Optimization:

The strategy is built with fully customizable input parameters for each indicator (MACD lengths, Kijun-sen period, ATR period, ATR multiplier, and Risk-to-Reward ratio). This allows users to fine-tune the strategy for different assets, timeframes, and market conditions, facilitating robust backtesting and optimization.

Disclaimer: Trading involves substantial risk and is not suitable for all investors. Past performance is not indicative of future results. This strategy is provided for educational and informational purposes only. Always use proper risk management and conduct your own due diligence.

Volatility Bias ModelVolatility Bias Model

Overview

Volatility Bias Model is a purely mathematical, non-indicator-based trading system that detects directional probability shifts during high volatility market phases. Rather than relying on classic tools like RSI or moving averages, this strategy uses raw price behavior and clustering logic to determine potential breakout direction based on recent market bias.

How It Works

Over a defined lookback window (default 10 bars), the strategy counts how many candles closed in the same direction (i.e., bullish or bearish).

Simultaneously, it calculates the price range during that window.

If volatility is above a minimum threshold and a clear directional bias is detected (e.g., >60% of closes are bullish), a trade is opened in the direction of that bias.

This approach assumes that when high volatility is coupled with directional closing consistency, the market is probabilistically more likely to continue in that direction.

ATR-based stop-loss and take-profit levels are applied, and trades auto-exit after 20 bars if targets are not hit.

Key Features

- 100% non-indicator-based logic

- Statistically-driven directional bias detection

- Works across all timeframes (1H, 4H, 1D)

- ATR-based risk management

- No pyramiding, slippage and commissions included

- Compatible with real-world backtesting conditions

Realism & Assumptions

To make this strategy more aligned with actual trading environments, it includes 0.05% commission per trade and a 1-point slippage on every entry and exit.

Additionally, position sizing is set at 10% of a $10,000 starting capital, and no pyramiding is allowed.

These assumptions help avoid unrealistic backtest results and make the performance metrics more representative of live conditions.

Parameter Explanation

Bias Window (10 bars): Number of past candles used to evaluate directional closings

Bias Threshold (0.60): Required ratio of same-direction candles to consider a bias valid

Minimum Range (1.5%): Ensures the market is volatile enough to avoid noise

ATR Length (14): Used to dynamically define stop-loss and target zones

Risk-Reward Ratio (2.0): Take-profit is set at twice the stop-loss distance

Max Holding Bars (20): Trades are closed automatically after 20 bars to prevent stagnation

Originality Note

Unlike common strategies based on oscillators or moving averages, this script is built on pure statistical inference. It models the market as a probabilistic process and identifies directional intent based on historical closing behavior, filtered by volatility. This makes it a non-linear, adaptive model grounded in real-world price structure — not traditional technical indicators.

Disclaimer

This strategy is for educational and experimental purposes only. It does not constitute financial advice. Always perform your own analysis and test thoroughly before applying with real capital.

MACD + RSI + EMA + BB + ATR Day Trading StrategyEntry Conditions and Signals

The strategy implements a multi-layered filtering approach to entry conditions, requiring alignment across technical indicators, timeframes, and market conditions .

Long Entry Requirements

Trend Filter: Fast EMA (9) must be above Slow EMA (21), price must be above Fast EMA, and higher timeframe must confirm uptrend

MACD Signal: MACD line crosses above signal line, indicating increasing bullish momentum

RSI Condition: RSI below 70 (not overbought) but above 40 (showing momentum)

Volume & Volatility: Current volume exceeds 1.2x 20-period average and ATR shows sufficient market movement

Time Filter: Trading occurs during optimal hours (9:30-11:30 AM ET) when market volatility is typically highest

Exit Strategies

The strategy employs multiple exit mechanisms to adapt to changing market conditions and protect profits :

Stop Loss Management

Initial Stop: Placed at 2.0x ATR from entry price, adapting to current market volatility

Trailing Stop: 1.5x ATR trailing stop that moves up (for longs) or down (for shorts) as price moves favorably

Time-Based Exits: All positions closed by end of trading day (4:00 PM ET) to avoid overnight risk

Best Practices for Implementation

Settings

Chart Setup: 5-minute timeframe for execution with 15-minute chart for trend confirmation

Session Times: Focus on 9:30-11:30 AM ET trading for highest volatility and opportunity

Volatility Pulse with Dynamic ExitVolatility Pulse with Dynamic Exit

Overview

This strategy, Volatility Pulse with Dynamic Exit, is designed to capture impulsive price moves following volatility expansions, while ensuring risk is managed dynamically. It avoids trades during low-volatility periods and uses momentum confirmation to enter positions. Additionally, it features a time-based forced exit system to limit overexposure.

How It Works

A position is opened when the current ATR (Average True Range) significantly exceeds its 20-period average, signaling a volatility expansion.

To confirm the move is directional and not random noise, the strategy checks for momentum: the close must be above/below the close of 20 bars ago.

Low volatility zones are filtered out to avoid chop and poor trade entries.

Upon entry, a dynamic stop-loss is set at 1x ATR, while take-profit is set at 2x ATR, offering a 2:1 reward-to-risk ratio.

If the position remains open for more than 42 bars, it is forcefully closed, even if targets are not hit. This prevents long-lasting, stagnant trades.

Key Features

✅ Volatility-based breakout detection

✅ Momentum confirmation filter

✅ Dynamic stop-loss and take-profit based on real-time ATR

✅ Time-based forced exit (42 bars max holding)

✅ Low-volatility environment filter

✅ Realistic settings with 0.05% commission and slippage included

Parameters Explanation

ATR Length (14): Captures recent volatility over ~2 weeks (14 candles).

Momentum Lookback (20): Ensures meaningful price move confirmation.

Volatility Expansion Threshold (0.5x): Strategy activates only when ATR is at least 50% above its average.

Minimum ATR Filter (1.0x): Avoids entries in tight, compressed market ranges.

Max Holding (42 bars): Trades are closed after 42 bars if no exit signal is triggered.

Risk-Reward (2.0x): Aiming for 2x ATR as profit for every 1x ATR risk.

Originality Note

While volatility and momentum have been used separately in many strategies, this script combines both with a time-based dynamic exit system. This exit rule, combined with an ATR-based filter to exclude low-activity periods, gives the system a practical edge in real-world use. It avoids classic rehashes and integrates real trading constraints for better applicability.

Disclaimer

This is a research-focused trading strategy meant for backtesting and educational purposes. Always use proper risk management and perform due diligence before applying to real funds.

magic wand STSM"Magic Wand STSM" Strategy: Trend-Following with Dynamic Risk Management

Overview:

The "Magic Wand STSM" (Supertrend & SMA Momentum) is an automated trading strategy designed to identify and capitalize on sustained trends in the market. It combines a multi-timeframe Supertrend for trend direction and potential reversal signals, along with a 200-period Simple Moving Average (SMA) for overall market bias. A key feature of this strategy is its dynamic position sizing based on a user-defined risk percentage per trade, and a built-in daily and monthly profit/loss tracking system to manage overall exposure and prevent overtrading.

How it Works (Underlying Concepts):

Multi-Timeframe Trend Confirmation (Supertrend):

The strategy uses two Supertrend indicators: one on the current chart timeframe and another on a higher timeframe (e.g., if your chart is 5-minute, the higher timeframe Supertrend might be 15-minute).

Trend Identification: The Supertrend's direction output is crucial. A negative direction indicates a bearish trend (price below Supertrend), while a positive direction indicates a bullish trend (price above Supertrend).

Confirmation: A core principle is that trades are only considered when the Supertrend on both the current and the higher timeframe align in the same direction. This helps to filter out noise and focus on stronger, more confirmed trends. For example, for a long trade, both Supertrends must be indicating a bearish trend (price below Supertrend line, implying an uptrend context where price is expected to stay above/rebound from Supertrend). Similarly, for short trades, both must be indicating a bullish trend (price above Supertrend line, implying a downtrend context where price is expected to stay below/retest Supertrend).

Trend "Readiness": The strategy specifically looks for situations where the Supertrend has been stable for a few bars (checking barssince the last direction change).

Long-Term Market Bias (200 SMA):

A 200-period Simple Moving Average is plotted on the chart.

Filter: For long trades, the price must be above the 200 SMA, confirming an overall bullish bias. For short trades, the price must be below the 200 SMA, confirming an overall bearish bias. This acts as a macro filter, ensuring trades are taken in alignment with the broader market direction.

"Lowest/Highest Value" Pullback Entries:

The strategy employs custom functions (LowestValueAndBar, HighestValueAndBar) to identify specific price action within the recent trend:

For Long Entries: It looks for a "buy ready" condition where the price has found a recent lowest point within a specific number of bars since the Supertrend turned bearish (indicating an uptrend). This suggests a potential pullback or consolidation before continuation. The entry trigger is a close above the open of this identified lowest bar, and also above the current bar's open.

For Short Entries: It looks for a "sell ready" condition where the price has found a recent highest point within a specific number of bars since the Supertrend turned bullish (indicating a downtrend). This suggests a potential rally or consolidation before continuation downwards. The entry trigger is a close below the open of this identified highest bar, and also below the current bar's open.

Candle Confirmation: The strategy also incorporates a check on the candle type at the "lowest/highest value" bar (e.g., closevalue_b < openvalue_b for buy signals, meaning a bearish candle at the low, suggesting a potential reversal before a buy).

Risk Management and Position Sizing:

Dynamic Lot Sizing: The lotsvalue function calculates the appropriate position size based on your Your Equity input, the Risk to Reward ratio, and your risk percentage for your balance % input. This ensures that the capital risked per trade remains consistent as a percentage of your equity, regardless of the instrument's volatility or price. The stop loss distance is directly used in this calculation.

Fixed Risk Reward: All trades are entered with a predefined Risk to Reward ratio (default 2.0). This means for every unit of risk (stop loss distance), the target profit is rr times that distance.

Daily and Monthly Performance Monitoring:

The strategy tracks todaysWins, todaysLosses, and res (daily net result) in real-time.

A "daily profit target" is implemented (day_profit): If the daily net result is very favorable (e.g., res >= 4 with todaysLosses >= 2 or todaysWins + todaysLosses >= 8), the strategy may temporarily halt trading for the remainder of the session to "lock in" profits and prevent overtrading during volatile periods.

A "monthly stop-out" (monthly_trade) is implemented: If the lres (overall net result from all closed trades) falls below a certain threshold (e.g., -12), the strategy will stop trading for a set period (one week in this case) to protect capital during prolonged drawdowns.

Trade Execution:

Entry Triggers: Trades are entered when all buy/sell conditions (Supertrend alignment, SMA filter, "buy/sell situation" candle confirmation, and risk management checks) are met, and there are no open positions.

Stop Loss and Take Profit:

Stop Loss: The stop loss is dynamically placed at the upTrendValue for long trades and downTrendValue for short trades. These values are derived from the Supertrend indicator, which naturally adjusts to market volatility.

Take Profit: The take profit is calculated based on the entry price, the stop loss, and the Risk to Reward ratio (rr).

Position Locks: lock_long and lock_short variables prevent immediate re-entry into the same direction once a trade is initiated, or after a trend reversal based on Supertrend changes.

Visual Elements:

The 200 SMA is plotted in yellow.

Entry, Stop Loss, and Take Profit lines are plotted in white, red, and green respectively when a trade is active, with shaded areas between them to visually represent risk and reward.

Diamond shapes are plotted at the bottom of the chart (green for potential buy signals, red for potential sell signals) to visually indicate when the buy_sit or sell_sit conditions are met, along with other key filters.

A comprehensive trade statistics table is displayed on the chart, showing daily wins/losses, daily profit, total deals, and overall profit/loss.

A background color indicates the active trading session.

Ideal Usage:

This strategy is best applied to instruments with clear trends and sufficient liquidity. Users should carefully adjust the Your Equity, Risk to Reward, and risk percentage inputs to align with their individual risk tolerance and capital. Experimentation with different ATR Length and Factor values for the Supertrend might be beneficial depending on the asset and timeframe.

SMA Backtest Optimizer [Mr_Rakun]The SMA Backtest Optimizer is a powerful Pine Script tool designed to systematically analyze and compare various Simple Moving Average (SMA) periods to identify the most profitable configuration for trading strategies. This indicator tests multiple SMA periods (from 10 to 100) using a crossover strategy where buys occur when price crosses above the SMA and sells when price crosses below it.

Key Features:

Tests 10 different SMA periods to determine optimal settings

Calculates profit/loss based on a defined starting capital

Tracks total profit and number of trades for each period

Visually highlights the best performing SMA on your chart

Displays comprehensive results in an easy-to-read table

Labels the chart with key performance metrics

This code serves as a core framework that traders can customize for their specific needs. You can easily modify the strategy parameters, test different technical indicators, adjust capital settings, or implement more complex entry/exit rules. The optimization methodology can be applied to virtually any trading approach you wish to evaluate.

Feel free to adapt this framework to test your own trading ideas and discover which parameters work best in different market conditions.

CANX MA Crossover© CanxStixTrader

Moving average crossover systems measure drift in the market. They are great strategies for time-limited traders. KEEP IT SIMPLE

This strategy works both for buys and sells using the reaction line to guide your position against the reactions.

HOW TO USE THE INDICATOR

1) Choose your market and timeframe.

2) Choose the length.

3) Choose the multiplier.

4) Choose if the strategy is long-only or bidirectional (longs & shorts).

TIPS

The strategy works best in bullish markets as that is the primary direction that market such as stocks, indexes and metals like to move.

- Increase the multiplier to reduce whipsaws

- Increase the length to take fewer trades

- Decrease the length to take more trades

- Try a Long-Only strategy to see if that performs better.

The base set up when you load the indicator is for the 1 minute chart on gold. We found that it also works well on the US Indexes. For other markets you may need to change the length and multiplier to suit the market and back test its results.

EMA 10/20/50 Alignment Strategy### 📘 **Strategy Name**

**EMA 10/20/50 Trend Alignment Strategy**

---

### 📝 **Description (for Publishing)**

This strategy uses the alignment of Exponential Moving Averages (EMAs) to identify strong bullish trends. It enters a long position when the short-term EMA is above the mid-term EMA, which is above the long-term EMA — a classic sign of trend strength.

#### 🔹 Entry Criteria:

* **EMA10 > EMA20 > EMA50**: A bullish alignment that signals momentum in an upward direction.

* The strategy enters a **long position** when this alignment occurs.

#### 🔹 Exit Criteria:

* The long position is closed when the EMA alignment breaks (i.e., the trend weakens or reverses).

#### 🔹 Additional Features:

* Includes a **date range filter**, allowing you to backtest the strategy over a specific period.

* Uses **100% of available capital** for each trade (position size auto-scales with account balance).

* No short positions, stop loss, or take profit are applied — this is a trend-following strategy meant to ride bullish moves.

---

### ✅ Best For:

* Traders looking for a **simple, trend-based entry system**

* Testing price momentum strategies during specific market regimes

* Visualizing EMA stacking patterns in historical data

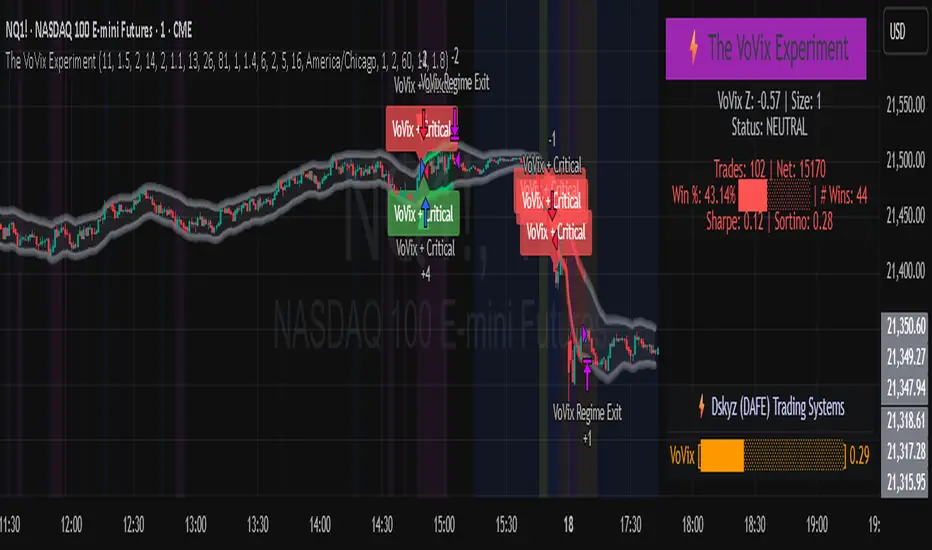

The VoVix Experiment The VoVix Experiment

The VoVix Experiment is a next-generation, regime-aware, volatility-adaptive trading strategy for futures, indices, and more. It combines a proprietary VoVix (volatility-of-volatility) anomaly detector with price structure clustering and critical point logic, only trading when multiple independent signals align. The system is designed for robustness, transparency, and real-world execution.

Logic:

VoVix Regime Engine: Detects pre-move volatility anomalies using a fast/slow ATR ratio, normalized by Z-score. Only trades when a true regime spike is detected, not just random volatility.

Cluster & Critical Point Filters: Price structure and volatility clustering must confirm the VoVix signal, reducing false positives and whipsaws.

Adaptive Sizing: Position size scales up for “super-spikes” and down for normal events, always within user-defined min/max.

Session Control: Trades only during user-defined hours and days, avoiding illiquid or high-risk periods.

Visuals: Aurora Flux Bands (From another Original of Mine (Options Flux Flow): glow and change color on signals, with a live dashboard, regime heatmap, and VoVix progression bar for instant insight.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 15 min (but works on all timeframes)

Order size: Adaptive, 1–2 contracts

Session: 5:00–15:00 America/Chicago (default, fully adjustable)

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for MNQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Forward Testing: (This is no guarantee. I've provided these results to show that executions perform as intended. Test were done on Tradovate)

ALL TRADES

Gross P/L: $12,907.50

# of Trades: 64

# of Contracts: 186

Avg. Trade Time: 1h 55min 52sec

Longest Trade Time: 55h 46min 53sec

% Profitable Trades: 59.38%

Expectancy: $201.68

Trade Fees & Comm.: $(330.95)

Total P/L: $12,576.55

Winning Trades: 59.38%

Breakeven Trades: 3.12%

Losing Trades: 37.50%

Link: www.dropbox.com

Inputs & Tooltips

VoVix Regime Execution: Enable/disable the core VoVix anomaly detector.

Volatility Clustering: Require price/volatility clusters to confirm VoVix signals.

Critical Point Detector: Require price to be at a statistically significant distance from the mean (regime break).

VoVix Fast ATR Length: Short ATR for fast volatility detection (lower = more sensitive).

VoVix Slow ATR Length: Long ATR for baseline regime (higher = more stable).

VoVix Z-Score Window: Lookback for Z-score normalization (higher = smoother, lower = more reactive).

VoVix Entry Z-Score: Minimum Z-score for a VoVix spike to trigger a trade.

VoVix Exit Z-Score: Z-score below which the regime is considered decayed (exit).

VoVix Local Max Window: Bars to check for local maximum in VoVix (higher = stricter).

VoVix Super-Spike Z-Score: Z-score for “super” regime events (scales up position size).

Min/Max Contracts: Adaptive position sizing range.

Session Start/End Hour: Only trade between these hours (exchange time).

Allow Weekend Trading: Enable/disable trading on weekends.

Session Timezone: Timezone for session filter (e.g., America/Chicago for CME).

Show Trade Labels: Show/hide entry/exit labels on chart.

Flux Glow Opacity: Opacity of Aurora Flux Bands (0–100).

Flux Band EMA Length: EMA period for band center.

Flux Band ATR Multiplier: Width of bands (higher = wider).

Compliance & Transparency

* No hidden logic, no repainting, no pyramiding.

* All signals, sizing, and exits are fully explained and visible.

* Backtest settings are stricter than most real accounts.

* All visuals are directly tied to the strategy logic.

* This is not a mashup or cosmetic overlay; every component is original and justified.

Disclaimer

Trading is risky. This script is for educational and research purposes only. Do not trade with money you cannot afford to lose. Past performance is not indicative of future results. Always test in simulation before live trading.

Proprietary Logic & Originality Statement

This script, “The VoVix Experiment,” is the result of original research and development. All core logic, algorithms, and visualizations—including the VoVix regime detection engine, adaptive execution, volatility/divergence bands, and dashboard—are proprietary and unique to this project.

1. VoVix Regime Logic

The concept of “volatility of volatility” (VoVix) is an original quant idea, not a standard indicator. The implementation here (fast/slow ATR ratio, Z-score normalization, local max logic, super-spike scaling) is custom and not found in public TradingView scripts.

2. Cluster & Critical Point Logic

Volatility clustering and “critical point” detection (using price distance from a rolling mean and standard deviation) are general quant concepts, but the way they are combined and filtered here is unique to this script. The specific logic for “clustered chop” and “critical point” is not a copy of any public indicator.

3. Adaptive Sizing

The adaptive sizing logic (scaling contracts based on regime strength) is custom and not a standard TradingView feature or public script.

4. Time Block/Session Control

The session filter is a common feature in many strategies, but the implementation here (with timezone and weekend control) is written from scratch.

5. Aurora Flux Bands (From another Original of Mine (Options Flux Flow)

The “glowing” bands are inspired by the idea of volatility bands (like Bollinger Bands or Keltner Channels), but the visual effect, color logic, and integration with regime signals are original to this script.

6. Dashboard, Watermark, and Metrics

The dashboard, real-time Sharpe/Sortino, and VoVix progression bar are all custom code, not copied from any public script.

What is “standard” or “common quant practice”?

Using ATR, EMA, and Z-score are standard quant tools, but the way they are combined, filtered, and visualized here is unique. The structure and logic of this script are original and not a mashup of public code.

This script is 100% original work. All logic, visuals, and execution are custom-coded for this project. No code or logic is directly copied from any public or private script.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

REVELATIONS (VoVix - PoC) REVELATIONS (VoVix - POC): True Regime Detection Before the Move

Let’s not sugarcoat it: Most strategies on TradingView are recycled—RSI, MACD, OBV, CCI, Stochastics. They all lag. No matter how many overlays you stack, every one of these “standard” indicators fires after the move is underway. The retail crowd almost always gets in late. That’s never been enough for my team, for DAFE, or for anyone who’s traded enough to know the real edge vanishes by the time the masses react.

How is this different?

REVELATIONS (VoVix - POC) was engineered from raw principle, structured to detect pre-move regime change—before standard technicals even light up. We built, tested, and refined VoVix to answer one hard question:

What if you could see the spike before the trend?

Here’s what sets this system apart, line-by-line:

o True volatility-of-volatility mathematics: It’s not just "ATR of ATR" or noise smoothing. VoVix uses normalized, multi-timeframe v-vol spikes, instantly detecting orderbook stress and "outlier" market events—before the chart shows them as trends.

o Purist regime clustering: Every trade is enabled only during coordinated, multi-filter regime stress. No more signals in meaningless chop.

o Nonlinear entry logic: No trade is ever sent just for a “good enough” condition. Every entry fires only if every requirement is aligned—local extremes, super-spike threshold, regime index, higher timeframe, all must trigger in sync.

o Adaptive position size: Your contracts scale up with event strength. Tiny size during nominal moves, max leverage during true regime breaks—never guesswork, never static exposure.

o All exits governed by regime decay logic: Trades are closed not just on price targets but at the precise moment the market regime exhausts—the hardest part of systemic trading, now solved.

How this destroys the lag:

Standard indicators (RSI, MACD, OBV, CCI, and even most “momentum” overlays) simply tell you what already happened. VoVix triggers as price structure transitions—anyone running these generic scripts will trade behind the move while VoVix gets in as stress emerges. Real alpha comes from anticipation, not confirmation.

The visuals only show what matters:

Top right, you get a live, live quant dashboard—regime index, current position size, real-time performance (Sharpe, Sortino, win rate, and wins). Bottom right: a VoVix "engine bar" that adapts live with regime stress. Everything you see is a direct function of logic driving this edge—no cosmetics, no fake momentum.

Inputs/Signals—explained carefully for clarity:

o ATR Fast Length & ATR Slow Length:

These are the heart of VoVix’s regime sensing. Fast ATR reacts to sharp volatility; Slow ATR is stability baseline. Lower Fast = reacts to every twitch; higher Slow = requires more persistent, “real” regime shifts.

Tip: If you want more signals or faster markets, lower ATR Fast. To eliminate noise, raise ATR Slow.

o ATR StdDev Window: Smoothing for volatility-of-volatility normalization. Lower = more jumpy, higher = only the cleanest spikes trigger.

Tip: Shorten for “jumpy” assets, raise for indices/futures.

o Base Spike Threshold: Think of this as your “minimum event strength.” If the current move isn’t volatile enough (normalized), no signal.

Tip: Higher = only biggest moves matter. Lower for more signals but more potential noise.

o Super Spike Multiplier: The “are you sure?” test—entry only when the current spike is this multiple above local average.

Tip: Raise for ultra-selective/swing-trading; lower for more active style.

Regime & MultiTF:

o Regime Window (Bars):

How many bars to scan for regime cluster “events.” Short for turbo markets, long for big swings/trends only.

o Regime Event Count: Only trade when this many spikes occur within the Regime Window—filters for real stress, not isolated ticks.

Tip: Raise to only ever trade during true breakouts/crashes.

o Local Window for Extremes:

How many bars to check that a spike is a local max.

Tip: Raise to demand only true, “clearest” local regime events; lower for early triggers.

o HTF Confirm:

Higher timeframe regime confirmation (like 45m on an intraday chart). Ensures any event you act on is visible in the broader context.

Tip: Use higher timeframes for only major moves; lower for scalping or fast regimes.

Adaptive Sizing:

o Max Contracts (Adaptive): The largest size your system will ever scale to, even on extreme event.

Tip: Lower for small accounts/conservative risk; raise on big accounts or when you're willing to go big only on outlier events.

o Min Contracts (Adaptive): The “toe-in-the-water.” Smallest possible trade.

Tip: Set as low as your broker/exchange allows for safety, or higher if you want to always have meaningful skin in the game.

Trade Management:

o Stop %: Tightness of your stop-loss relative to entry. Lower for tighter/safer, higher for more breathing room at cost of greater drawdown.

o Take Profit %: How much you'll hold out for on a win. Lower = more scalps. Higher = only run with the best.

o Decay Exit Sensitivity Buffer: Regime index must dip this far below the trading threshold before you exit for “regime decay.”

Tip: 0 = exit as soon as stress fails, higher = exits only on stronger confirmation regime is over.

o Bars Decay Must Persist to Exit: How long must decay be present before system closes—set higher to avoid quick fades and whipsaws.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Tip: Set to 1 for instant regime exit; raise for extra confirmation (less whipsaw risk, exits held longer).

________________________________________

Bottom line: Tune the sensitivity, selectivity, and risk of REVELATIONS by these inputs. Raise thresholds and windows for only the best, most powerful signals (institutional style); lower for activity (scalpers, fast cryptos, signals in constant motion). Sizing is always adaptive—never static or martingale. Exits are always based on both price and regime health. Every input is there for your control, not to sell “complexity.” Use with discipline, and make it your own.

This strategy is not just a technical achievement: It’s a statement about trading smarter, not just more.

* I went back through the code to make sure no the strategy would not suffer from repainting, forward looking, or any frowned upon loopholes.

Disclaimer:

Trading is risky and carries the risk of substantial loss. Do not use funds you aren’t prepared to lose. This is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

Expect more: We’ll keep pushing the standard, keep evolving the bar until “quant” actually means something in the public code space.

Use with clarity, use with discipline, and always trade your edge.

— Dskyz , for DAFE Trading Systems

Order Block with BoSHere’s a professional and concise description you can use for publishing your **TradingView script** titled **"Order Block with BoS"**:

---

### 📌 **Description for TradingView Publication:**

**"Order Block with Break of Structure (BoS)"** is a powerful price action-based indicator designed to identify potential reversal zones and momentum shifts using **Order Block** detection combined with **Break of Structure (BoS)** confirmation.

### 🔍 **Key Features:**

* **Order Block Detection**: Highlights bullish and bearish order blocks using precise candle structure logic.

* **Break of Structure (BoS)**: Confirms structural breaks above swing highs or below swing lows to validate potential trend continuation or reversal.

* **Dynamic ATR Filter**: Uses a 14-period ATR with dynamic thresholds to confirm significant moves, filtering out weak breakouts.

* **Visual Aids**:

* Color-coded **boxes** to mark detected Order Blocks.

* **Arrows** at BoS confirmation points when ATR confirms strong momentum.

* Optional **dashed BoS lines** to show where price broke structure.

### ⚙️ **Customizable Inputs**:

* `Swing Length`: Defines the sensitivity of swing high/low detection.

* `Show Break of Structure`: Toggle on/off BoS confirmation lines.

* `Candle Lookback`: Number of historical candles to consider.

This indicator is ideal for traders who incorporate **smart money concepts**, **market structure analysis**, or **institutional order flow** strategies.

---

Would you like me to help write the **strategy** version of this or translate the description into another language for international audiences?

Stochastic RSI with MTF TableShort Description of the Script

The provided Pine Script indicator, titled "Stochastic RSI with MTF Table," calculates and displays the Stochastic RSI for the current timeframe and multiple other timeframes (5m, 15m, 30m, 60m, 240m, and daily). The Stochastic RSI is a momentum indicator that blends the Relative Strength Index (RSI) and Stochastic Oscillator to identify overbought and oversold conditions, as well as potential trend reversals via K and D line crossovers.

Key features of the script include:

Inputs: Customizable parameters such as K smoothing (default 3), D smoothing (default 3), RSI length (default 14), Stochastic length (default 14), source price (default close), and overbought/oversold levels (default 80/20).

MTF Table: A table displays the Stochastic RSI status for each timeframe:

"OB" (overbought) if K > 80, "OS" (oversold) if K < 20, or "N" (neutral) otherwise.

Crossovers: "K↑D" for bullish (K crosses above D) and "K↓D" for bearish (K crosses below D).

Visualization: Plots the K and D lines for the current timeframe, with horizontal lines at 80 (overbought), 50 (middle), and 20 (oversold), plus a background fill for clarity.

Table Position: Configurable to appear in one of four chart corners (default: top-right).

This indicator helps traders assess momentum across multiple timeframes simultaneously, aiding in the identification of trend strength and potential entry/exit points.

Trading Strategy with 50EMA and 200EMA for Highest Winning Rate

To create a strategy with the best probability of a high winning rate using the Stochastic RSI MTF indicator alongside the 50-period Exponential Moving Average (50EMA) and 200-period Exponential Moving Average (200EMA), we can combine trend identification with momentum-based entry timing. The 50EMA and 200EMA are widely used to determine medium- and long-term trends, while the Stochastic RSI MTF table provides multi-timeframe momentum signals. Here’s the strategy:

1. Determine the Overall Trend

Bullish Trend: The 50EMA is above the 200EMA on the current timeframe (e.g., daily or 60m chart). This suggests an uptrend, often associated with a "Golden Cross."

Bearish Trend: The 50EMA is below the 200EMA on the current timeframe. This indicates a downtrend, often linked to a "Death Cross."

Implementation: Plot the 50EMA and 200EMA on your chart and visually confirm their relative positions.

2. Identify Entry Signals Using the Stochastic RSI MTF Table

In a Bullish Trend (50EMA > 200EMA):

Look for timeframes in the MTF table showing:

Oversold (OS): K < 20, indicating a potential pullback in the uptrend where price may rebound.

Bullish Crossover (K↑D): K crosses above D, signaling rising momentum and a potential entry point.

Example: If the 60m and 240m timeframes show "OS" or "K↑D," this could be a buy signal.

In a Bearish Trend (50EMA < 200EMA):

Look for timeframes in the MTF table showing:

Overbought (OB): K > 80, suggesting a rally in the downtrend where price may reverse downward.

Bearish Crossover (K↓D): K crosses below D, indicating declining momentum and a potential short entry.

Example: If the 30m and daily timeframes show "OB" or "K↓D," this could be a sell/short signal.

Current Timeframe Check: Use the plotted K and D lines on your trading timeframe for precise entry timing (e.g., confirm a K↑D crossover on a 60m chart for a long trade).

3. Confirm Signals Across Multiple Timeframes

Strengthen the Signal: A higher winning rate is more likely when multiple timeframes align with the trend and signal. For instance:

Bullish trend + "OS" or "K↑D" on 60m, 240m, and daily = strong buy signal.

Bearish trend + "OB" or "K↓D" on 15m, 60m, and 240m = strong sell signal.

Prioritize Higher Timeframes: Signals from the 240m or daily timeframe carry more weight due to their indication of broader trends, increasing reliability.

4. Set Stop-Loss and Take-Profit Levels

Long Trades (Bullish):

Stop-Loss: Place below the most recent swing low or below the 50EMA, whichever is closer, to protect against trend reversals.

Take-Profit: Target a key resistance level or use a risk-reward ratio (e.g., 2:1 or 3:1) based on the stop-loss distance.

Short Trades (Bearish):

Stop-Loss: Place above the most recent swing high or above the 50EMA, whichever is closer.

Take-Profit: Target a key support level or apply a similar risk-reward ratio.

Trailing Stop Option: As the trend progresses, trail the stop below the 50EMA (for longs) or above it (for shorts) to lock in profits.

5. Risk Management

Position Sizing: Risk no more than 1-2% of your trading capital per trade to minimize losses from false signals.

Volatility Consideration: Adjust stop-loss distances and position sizes based on the asset’s volatility (e.g., wider stops for volatile stocks or crypto).

Avoid Overtrading: Wait for clear alignment between the EMA trend and MTF signals to avoid low-probability setups.

Example Scenario

Chart: 60-minute timeframe.

Trend: 50EMA > 200EMA (bullish).

MTF Table: 60m shows "OS," 240m shows "K↑D," and daily is "N."

Action: Enter a long position when the 60m K line crosses above D, confirming the table signal.

Stop-Loss: Below the recent 60m swing low (e.g., 2% below entry).

Take-Profit: At the next resistance level or a 3:1 reward-to-risk ratio.

Outcome: High probability of success due to trend alignment and multi-timeframe confirmation.

Why This Strategy Works

Trend Following: Trading in the direction of the 50EMA/200EMA trend reduces the risk of fighting the market’s momentum.

Momentum Timing: The Stochastic RSI MTF table pinpoints pullbacks or reversals within the trend, improving entry timing.

Multi-Timeframe Confirmation: Alignment across timeframes filters out noise, increasing the win rate.

Risk Control: Defined stop-loss and position sizing protect against inevitable losses.

Caveats

No strategy guarantees a 100% win rate; false signals can occur, especially in choppy markets.

Test this strategy on historical data or a demo account to verify its effectiveness for your asset and timeframe.

This approach leverages the strengths of both trend-following (EMA) and momentum (Stochastic RSI) tools, aiming for a high-probability, disciplined trading system.

UTSStrategyHelperLibrary "UTSStrategyHelper"

TODO: add library description here

stopLossPrice(sig, atr, factor, isLong)

Calculates the stop loss price using a distance determined by ATR multiplied by a factor. Example for Long trade SL: PRICE - (ATR * factor).

Parameters:

sig (float)

atr (float) : (float): The value of the atr.

factor (float)

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

takeProfitPrice(sig, atr, factor, isLong)

Calculates the take profit price using a distance determined by ATR multiplied by a factor. Example for Long trade TP: PRICE + (ATR * factor). When take profit price is reached usually 50 % of the position is closed and the other 50 % get a trailing stop assigned.

Parameters:

sig (float)

atr (float) : (float): The value of the atr.

factor (float)

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

trailingStopPrice(initialStopPrice, atr, factor, priceSource, isLong)

Calculates a trailing stop price using a distance determined by ATR multiplied by a factor. It takes an initial price and follows the price closely if it changes in a favourable way.

Parameters:

initialStopPrice (float) : (float): The initial stop price which, for consistency also should be ATR * factor behind price: e.g. Long trade: PRICE - (ATR * factor)

atr (float) : (float): The value of the atr. Ideally the ATR value at trade open is taken and used for subsequent calculations.

factor (float)

priceSource (float) : (float): The current price.

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

hasGreaterPositionSize(positionSize)

Determines if the strategy's position size has grown since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasSmallerPositionSize(positionSize)

Determines if the strategy's position size has decreased since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasUnchangedPositionSize(positionSize)

Determines if the strategy's position size has changed since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

exporthasLongPosition(positionSize)

Determines if the strategy has an open long position.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasShortPosition(positionSize)

Determines if the strategy has an open short position.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasAnyPosition(positionSize)

Determines if the strategy has any open position, regardless of short or long.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasSignal(value)

Determines if the given argument contains a valid value (means not 'na').

Parameters:

value (float) : (float): The actual value.

Returns: (bool): A boolean value.

Camarilla Pivot Plays█ OVERVIEW

This indicator implements the Camarilla Pivot Points levels and a system for suggesting particular plays. It only calculates and shows the 3rd, 4th, and 6th levels, as these are the only ones used by the system. In total, there are 12 possible plays, grouped into two groups of six. The algorithm constantly evaluates conditions for entering and exiting the plays and indicates them in real time, also triggering user-configurable alerts.

█ CREDITS

The Camarilla pivot plays are defined in a strategy developed by Thor Young, and the whole system is explained in his book "A Complete Day Trading System" . The indicator is published with his permission, and he is a user of it. The book is not necessary in order to understand and use the indicator; this description contains sufficient information to use it effectively.

█ FEATURES

Automatically draws plays, suggesting an entry, stop-loss, and maximum target

User can set alerts on chosen ticker to call these plays, even when not currently viewing them

Highly configurable via many options

Works for US/European stocks and US futures (at least)

Works correctly on both RTH and ETH charts

Automatically switches between RTH and ETH data

Optionally also shows the "other" set of pivots (RTH vs ETH data)

Configurable behaviour in the pre-market, not active in the post-market

Configurable sensitivity of the play detection algorithm

Can also show weekly and monthly Camarilla pivots

Well-documented options tooltips

Sensible defaults which are suitable for immediate use

Well-documented and high-quality open-source code for those who are interested

█ HOW TO USE

The defaults work well; at a minimum, just add the indicator and watch the plays being called. To avoid having to watch securities, by selecting the three dots next to the indicator name, you can set an alert on the indicator and choose to be alerted on play entry or exit events—or both. The following diagram shows several plays activated in the past (with the "Show past plays" option selected).

By default, the indicator draws plays 5 days back; this can be changed up to 20 days. The labels can be shifted left/right using the "label offset" option to avoid overlapping with other labels in this indicator or those of another indicator.

An information box at the top-right of the chart shows:

The data currently in use for the main pivots. This can switch in the pre-market if the H/L range exceeds the previous day's H/L, and if it does, you will see that switch at the time that it happens

Whether the current day's pivots are in a higher or lower range compared to the previous day's. This is based on the RTH close, so large moves in the post-market won't be reflected (there is an advanced option to change this)

The width of the value relationship in the current day compared to the previous day

The currently active play. If multiple plays are active in parallel, only the last activated one is shown

The resistance pivots are all drawn in the same colour (red by default), as are the support pivots (green by default). You can change the resistance and support colours, but it is not possible to have different colours for different levels of the same kind. Plays will always use the correct colour, drawing over the pivots. For example, R4 is red by default, but if a play treats R4 as a support, then the play will draw a green line (by default) over the red R4 line, thereby hiding it while the play is active.

There are a few advanced parameters; leave these as default unless you really know what they do. Please note the script is complicated—it does a lot. You might need to wait a few seconds while it (re)calculates on new tickers or when changing options. Give it time when first loading or changing options!

█ CONCEPTS

The indicator is focused around daily Camarilla pivots and implements 12 possible plays: 6 when in a higher range, 6 when in a lower range. The plays are labelled by two letters—the first indicates the range, the second indicates the play—as shown in this diagram:

The pivots can be calculated using only RTH (Regular Trading Hours) data, or ETH (Extended Trading Hours) data, which includes the pre-market and post-market. The indicator implements logic to automatically choose the correct data, based on the rules defined by the strategy. This is user-overridable. With the default options, ETH will be used when the H/L range in the previous day's post-market or current day's pre-market exceeds that of the previous day's regular market. In auto mode, the chosen pivots are considered the main pivots for that day and are the ones used for play evaluation. The "other" pivots can also be shown—"other" here meaning using ETH data when the main pivots use RTH data, and vice versa.

When displaying plays in the pre-market, since the RTH open is not yet known (and that value is needed to evaluate play pre-conditions), the pre-market open is used as a proxy for the RTH open. After the regular market opens, the correct RTH open is used to evaluate play conditions.

█ NOTE FOR FUTURES

Futures always use full ETH data in auto mode. Users may, however, wish to use the option "Always use RTH close," which uses the 3 p.m. Central Time (CME/Chicago) as a basis for the close in the pivot calculations (instead of the 4 p.m. actual close).

Futures don't officially have a pre-market or post-market like equities. Let's take ES on CME as an example (CME is in Chicago, so all times are Central Time, i.e., 1 hour behind Eastern Time). It trades from 17:00 Sunday to 16:00 Friday, with a daily pause between 16:00 and 17:00. However, most of the trading activity is done between 08:30 and 15:00 (Central), which you can tell from the volume spikes at those times, and this coincides with NYSE/NASDAQ regular hours (09:30–16:00 Eastern). So we define a pseudo-pre-market from 17:00 the previous day to 08:30 on the current day, then a pseudo-regular market from 08:30 to 15:00, then a pseudo-post-market from 15:00 to 16:00.

The indicator then works exactly the same as with equities—all the options behave the same, just with different session times defined for the pre-, regular, and post-market, with "RTH" meaning just the regular market and "ETH" meaning all three. The only difference from equities is that the auto calculation mode always uses ETH instead of switching based on ETH range compared to RTH range. This is so users who just leave all the defaults are not confused by auto-switching of the calculation mode; normally you'll want the pivots based on all the (ETH) data. However, both "Force RTH" and "Use RTH close with ETH data" work the same as with equities—so if, in the calculations, you really want to only use RTH data, or use all ETH H/L data but use the RTH close (at 15:00), you can.

█ LIMITATIONS

The pivots are very close to those shown in DAS Trader Pro. They are not to-the-cent exact, but within a few cents. The reasons are:

TradingView uses real-time data from CBOE One, so doesn't have access to full exchange data (unless you pay for it in TradingView), and

the close/high/low are taken from the intraday timeframe you are currently viewing, not daily data—which are very close, but often not exactly the same. For example, the high on the daily timeframe may differ slightly from the daily high you'll see on an intraday timeframe.

I have occasionally seen larger than a few cents differences in the pivots between these and DAS Trader Pro—this is always due to differences in data, for example a big spike in the data in TradingView but not in DAS Trader Pro, or vice versa. The more traded the stock is, the less the difference tends to be. Highly traded stocks are usually within a few cents. Less traded stocks may be more (for example, 30¢ difference in R4 is the highest I've seen). If it bothers you, official NYSE/NASDAQ data in TradingView is quite inexpensive (but even that doesn't make the 8am candle identical).

The 6th Camarilla level does not have a standard definition and may not match the level shown on other platforms. It does match the definition used by DAS Trader Pro.

The indicator is an intraday indicator (despite also being able to show weekly and monthly pivots on an intraday chart). It deactivates on a daily timeframe and higher. It is untested on sub-minute timeframes; you may encounter runtime errors on these due to various historical data referencing issues. Also, the play detection algorithm would likely be unpredictable on sub-minute timeframes. Therefore, sub-minute timeframes are formally unsupported.

The indicator was developed and tested for US/European stocks and US futures. It may or may not work as intended for stocks and futures in different locations. It does not work for other security types (e.g., crypto), where I have no evidence that the strategy has any relevance.

Best SMA FinderThis script, Best SMA Finder, is a tool designed to identify the most robust simple moving average (SMA) length for a given chart, based on historical backtest performance. It evaluates hundreds of SMA values (from 10 to 1000) and selects the one that provides the best balance between profitability, consistency, and trade frequency.

What it does:

The script performs individual backtests for each SMA length using either "Long Only" or "Buy & Sell" logic, as selected by the user. For each tested SMA, it computes:

- Total number of trades

- Profit Factor (total profits / total losses)

- Win Rate

- A composite Robustness Score, which integrates Profit Factor, number of trades (log-scaled), and win rate.

Only SMA configurations that meet the user-defined minimum trade count are considered valid. Among all valid candidates, the script selects the SMA length with the highest robustness score and plots it on the chart.

How to use it:

- Choose the strategy type: "Long Only" or "Buy & Sell"

- Set the minimum trade count to filter out statistically irrelevant results

- Enable or disable the summary stats table (default: enabled)

The selected optimal SMA is plotted on the chart in blue. The optional table in the top-right corner shows the corresponding SMA length, trade count, Profit Factor, Win Rate, and Robustness Score for transparency.

Key Features:

- Exhaustive SMA optimization across 991 values

- Customizable trade direction and minimum trade filters

- In-chart visualization of results via table and plotted optimal SMA

- Uses a custom robustness formula to rank SMA lengths

Use cases:

Ideal for traders who want to backtest and auto-select a historically effective SMA without manual trial-and-error. Useful for swing and trend-following strategies across different timeframes.

📌 Limitations:

- Not a full trading strategy with position sizing or stop-loss logic

- Only one entry per direction at a time is allowed

- Designed for exploration and optimization, not as a ready-to-trade system

This script is open-source and built entirely from original code and logic. It does not replicate any closed-source script or reuse significant external open-source components.

PowerHouse SwiftEdge AI v2.10 StrategyOverview

The PowerHouse SwiftEdge AI v2.10 Strategy is a sophisticated trading system designed to identify high-probability trade setups in forex, stocks, and cryptocurrencies. By combining multi-timeframe trend analysis, momentum signals, volume confirmation, and smart money concepts (Change of Character and Break of Structure ), this strategy offers traders a robust tool to capitalize on market trends while minimizing false signals. The strategy’s unique “AI” component analyzes trends across multiple timeframes to provide a clear, actionable dashboard, making it accessible for both novice and experienced traders. The strategy is fully customizable, allowing users to tailor its filters to their trading style.

What It Does

This strategy generates Buy and Sell signals based on a confluence of technical indicators and smart money concepts. It uses:

Multi-Timeframe Trend Analysis: Confirms the market’s direction by analyzing trends on the 1-hour (60M), 4-hour (240M), and daily (D) timeframes.

Momentum Filter: Ensures trades align with strong price movements to avoid choppy markets.

Volume Filter: Validates signals with above-average volume to confirm market participation.

Breakout Filter: Requires price to break key levels for added confirmation.

Smart Money Signals (CHoCH/BOS): Identifies reversals (CHoCH) and trend continuations (BOS) based on pivot points.

AI Trend Dashboard: Summarizes trend strength, confidence, and predictions across timeframes, helping traders make informed decisions without needing to analyze complex data manually.

The strategy also plots dynamic support and resistance trendlines, take-profit (TP) levels, and “Get Ready” signals to alert users of potential setups before they fully develop. Trades are executed with predefined take-profit and stop-loss levels for disciplined risk management.

How It Works

The strategy integrates multiple components to create a cohesive trading system:

Multi-Timeframe Trend Analysis:

The strategy evaluates trends on three timeframes (1H, 4H, Daily) using Exponential Moving Averages (EMA) and Volume-Weighted Average Price (VWAP). A trend is considered bullish if the price is above both the EMA and VWAP, bearish if below, or neutral otherwise.

Signals are only generated when the trend on the user-selected higher timeframe aligns with the trade direction (e.g., Buy signals require a bullish higher timeframe trend). This reduces noise and ensures trades follow the broader market context.

Momentum Filter:

Measures the percentage price change between consecutive bars and compares it to a volatility-adjusted threshold (based on the Average True Range ). This ensures trades are taken only during significant price movements, filtering out low-momentum conditions.

Volume Filter (Optional):

Checks if the current volume exceeds a long-term average and shows positive short-term volume change. This confirms strong market participation, reducing the risk of false breakouts.

Breakout Filter (Optional):

Requires the price to break above (for Buy) or below (for Sell) recent highs/lows, ensuring the signal aligns with a structural shift in the market.

Smart Money Concepts (CHoCH/BOS):

Change of Character (CHoCH): Detects potential reversals when the price crosses under a recent pivot high (for Sell) or over a recent pivot low (for Buy) with a bearish or bullish candle, respectively.

Break of Structure (BOS): Confirms trend continuations when the price breaks below a recent pivot low (for Sell) or above a recent pivot high (for Buy) with strong momentum.

These signals are plotted as horizontal lines with labels, making it easy to visualize key levels.

AI Trend Dashboard:

Combines trend direction, momentum, and volatility (ATR) across timeframes to calculate a trend score. Scores above 0.5 indicate an “Up” trend, below -0.5 indicate a “Down” trend, and otherwise “Neutral.”

Displays a table summarizing trend strength (as a percentage), AI confidence (based on trend alignment), and Cumulative Volume Delta (CVD) for market context.

A second table (optional) shows trend predictions for 1H, 4H, and Daily timeframes, helping traders anticipate future market direction.

Dynamic Trendlines:

Plots support and resistance lines based on recent swing lows and highs within user-defined periods (shortTrendPeriod, longTrendPeriod). These lines adapt to market conditions and are colored based on trend strength.

Why This Combination?

The PowerHouse SwiftEdge AI v2.10 Strategy is original because it seamlessly integrates traditional technical analysis (EMA, VWAP, ATR, volume) with smart money concepts (CHoCH, BOS) and a proprietary AI-driven trend analysis. Unlike standalone indicators, this strategy:

Reduces False Signals: By requiring confluence across trend, momentum, volume, and breakout filters, it minimizes trades in choppy or low-conviction markets.

Adapts to Market Context: The ATR-based momentum threshold adjusts dynamically to volatility, ensuring signals remain relevant in both trending and ranging markets.

Simplifies Decision-Making: The AI dashboard distills complex multi-timeframe data into a user-friendly table, eliminating the need for manual analysis.

Leverages Smart Money: CHoCH and BOS signals capture institutional price action patterns, giving traders an edge in identifying reversals and continuations.

The combination of these components creates a balanced system that aligns short-term trade entries with longer-term market trends, offering a unique blend of precision, adaptability, and clarity.

How to Use

Add to Chart:

Apply the strategy to your TradingView chart on a liquid symbol (e.g., EURUSD, BTCUSD, AAPL) with a timeframe of 60 minutes or lower (e.g., 15M, 60M).

Configure Inputs:

Pivot Length: Adjust the number of bars (default: 5) to detect pivot highs/lows for CHoCH/BOS signals. Higher values reduce noise but may delay signals.

Momentum Threshold: Set the base percentage (default: 0.01%) for momentum confirmation. Increase for stricter signals.

Take Profit/Stop Loss: Define TP and SL in points (default: 10 each) for risk management.

Higher/Lower Timeframe: Choose timeframes (60M, 240M, D) for trend filtering. Ensure the chart timeframe is lower than or equal to the higher timeframe.

Filters: Enable/disable momentum, volume, or breakout filters to suit your trading style.

Trend Periods: Set shortTrendPeriod (default: 30) and longTrendPeriod (default: 100) for trendline plotting. Keep below 2000 to avoid buffer errors.

AI Dashboard: Toggle Enable AI Market Analysis to show/hide the prediction table and adjust its position.

Interpret Signals:

Buy/Sell Labels: Green "Buy" or red "Sell" labels indicate trade entries with predefined TP/SL levels plotted.

Get Ready Signals: Yellow "Get Ready BUY" or orange "Get Ready SELL" labels warn of potential setups.

CHoCH/BOS Lines: Aqua (CHoCH Sell), lime (CHoCH Buy), fuchsia (BOS Sell), or teal (BOS Buy) lines mark key levels.

Trendlines: Green/lime (support) or fuchsia/purple (resistance) dashed lines show dynamic support/resistance.

AI Dashboard: Check the top-right table for trend strength, confidence, and CVD. The optional bottom table shows trend predictions (Up, Down, Neutral).

Backtest and Trade:

Use TradingView’s Strategy Tester to evaluate performance. Adjust TP/SL and filters based on results.

Trade manually based on signals or automate with TradingView alerts (set alerts for Buy/Sell labels).

Originality and Value

The PowerHouse SwiftEdge AI v2.10 Strategy stands out by combining multi-timeframe analysis, smart money concepts, and an AI-driven dashboard into a single, user-friendly system. Its adaptive momentum threshold, robust filtering, and clear visualizations empower traders to make confident decisions without needing advanced technical knowledge. Whether you’re a day trader or swing trader, this strategy provides a versatile, data-driven approach to navigating dynamic markets.

Important Notes:

Risk Management: Always use appropriate position sizing and risk management, as the strategy’s TP/SL levels are customizable.

Symbol Compatibility: Test on liquid symbols with sufficient historical data (at least 2000 bars) to avoid buffer errors.

Performance: Backtest thoroughly to optimize settings for your market and timeframe.

BTC Daily DCA CalculatorThe BTC Daily DCA Calculator is an indicator that calculates how much Bitcoin (BTC) you would own today by investing a fixed dollar amount daily (Dollar-Cost Averaging) over a user-defined period. Simply input your start date, end date, and daily investment amount, and the indicator will display a table on the last candle showing your total BTC, total invested, portfolio value, and unrealized yield (in USD and percentage).

Features

Customizable Inputs: Set the start date, end date, and daily dollar amount to simulate your DCA strategy.

Results Table: Displays on the last candle (top-right of the chart) with:

Total BTC: The accumulated Bitcoin from daily purchases.

Total Invested ($): The total dollars invested.

Portfolio Value ($): The current value of your BTC holdings.

Unrealized Yield ($): Your profit/loss in USD.

Unrealized Yield (%): Your profit/loss as a percentage.

Visual Markers: Green triangles below the chart mark each daily investment.

Overlay on Chart: The table and markers appear directly on the BTCUSD price chart for easy reference.

Daily Timeframe: Designed for Daily (1D) charts to ensure accurate calculations.

How to Use

Add the Indicator: Apply the indicator to a BTCUSD chart (e.g., Coinbase:BTCUSD, Binance:BTCUSDT).

Set Daily Timeframe: Ensure your chart is on the Daily (1D) timeframe, or the script will display an error.

Configure Inputs: Open the indicator’s Settings > Inputs tab and set:

Start Date: When to begin the DCA strategy (e.g., 2024-01-01).

End Date: When to end the strategy (e.g., 2025-04-27 or earlier).

Daily Investment ($): The fixed dollar amount to invest daily (e.g., $100).

View Results: Scroll to the last candle in your date range to see the results table in the top-right corner of the chart. Green triangles below the bars indicate investment days.

Settings

Start Date: Choose the start date for your DCA strategy (default: 2024-01-01).

End Date: Choose the end date (default: 2025-04-27). Must be after the start date and within available chart data.

Daily Investment ($): Set the daily investment amount (default: $100). Minimum is $0.01.

Notes

Timeframe: The indicator requires a Daily (1D) chart. Other timeframes will trigger an error.

Data: Ensure your BTCUSD chart has historical data for the selected date range. Use reliable pairs like Coinbase:BTCUSD or Binance:BTCUSDT.

Limitations: Does not account for trading fees or slippage. Future dates (beyond the current date) will not display results.

Performance: Works best with historical data. Free TradingView accounts may have limited historical data; consider premium for longer ranges.

TASC 2025.05 Trading The Channel█ OVERVIEW

This script implements channel-based trading strategies based on the concepts explained by Perry J. Kaufman in the article "A Test Of Three Approaches: Trading The Channel" from the May 2025 edition of TASC's Traders' Tips . The script explores three distinct trading methods for equities and futures using information from a linear regression channel. Each rule set corresponds to different market behaviors, offering flexibility for trend-following, breakout, and mean-reversion trading styles.

█ CONCEPTS

Linear regression

Linear regression is a model that estimates the relationship between a dependent variable and one or more independent variables by fitting a straight line to the observed data. In the context of financial time series, traders often use linear regression to estimate trends in price movements over time.

The slope of the linear regression line indicates the strength and direction of the price trend. For example, a larger positive slope indicates a stronger upward trend, and a larger negative slope indicates the opposite. Traders can look for shifts in the direction of a linear regression slope to identify potential trend trading signals, and they can analyze the magnitude of the slope to support trading decisions.

One caveat to linear regression is that most financial time series data does not follow a straight line, meaning a regression line cannot perfectly describe the relationships between values. Prices typically fluctuate around a regression line to some degree. As such, analysts often project ranges above and below regression lines, creating channels to model the expected extent of the data's variability. This strategy constructs a channel based on the method used in Kaufman's article. It measures the maximum distances from points on the linear regression line to historical price values, then adds those distances and the current slope to the regression points.

Depending on the trading style, traders might look for prices to move outside an established channel for breakout signals, or they might look for price action to reach extremes within the channel for potential mean reversion opportunities.

█ STRATEGY CALCULATIONS

Primary trade rules

This strategy implements three distinct sets of rules for trend, breakout, and mean-reversion trades based on the methods Kaufman describes in his article:

Trade the trend (Rule 1) : Open new positions when the sign of the slope changes, indicating a potential trend reversal. Close short trades and enter a long trade when the slope changes from negative to positive, and do the opposite when the slope changes from positive to negative.

Trade channel breakouts (Rule 2) : Open new positions when prices cross outside the linear regression channel for the current sample. Close short trades and enter a long trade when the price moves above the channel, and do the opposite when the price moves below the channel.

Trade within the channel (Rule 3) : Open new positions based on price values within the channel's range. Close short trades and enter a long trade when the price is near the channel's low, within a specified percentage of the channel's range, and do the opposite when the price is near the channel's high. With this rule, users can also filter the trades based on the channel's slope. When the filter is active, long positions are allowed only when the slope is positive, and short positions are allowed only when it is negative.

Position sizing

Kaufman's strategy uses specific trade sizes for equities and futures markets:

For an equities symbol, the number of shares traded is $10,000 divided by the current price.

For a futures symbol, the number of contracts traded is based on a volatility-adjusted formula that divides $25,000 by the product of the 20-bar average true range and the instrument's point value.

By default, this script automatically uses these sizes for its trade simulation on equities and futures symbols and does not simulate trading on other symbols. However, users can control position sizes from the "Settings/Properties" tab and enable trade simulation on other symbol types by selecting the "Manual" option in the script's "Position sizing" input.

Stop-loss

This strategy includes the option to place an accompanying stop-loss order for each trade, which users can enable from the "SL %" input in the "Settings/Inputs" tab. When enabled, the strategy places a stop-loss order at a specified percentage distance from the closing price where the entry order occurs, allowing users to compare how the strategy performs with added loss protection.

█ USAGE

This strategy adapts its display logic for the three trading approaches based on the rule selected in the "Trade rule" input:

For all rules, the script plots the linear regression slope in a separate pane. The plot is color-coded to indicate whether the current slope is positive or negative.

When the selected rule is "Trade the trend", the script plots triangles in the separate pane to indicate when the slope's direction changes from positive to negative or vice versa. Additionally, it plots a color-coded SMA on the main chart pane, allowing visual comparison of the slope to directional changes in a moving average.

When the rule is "Trade channel breakouts" or "Trade within the channel", the script draws the current period's linear regression channel on the main chart pane, and it plots bands representing the history of the channel values from the specified start time onward.

When the rule is "Trade within the channel", the script plots overbought and oversold zones between the bands based on a user-specified percentage of the channel range to indicate the value ranges where new trades are allowed.

Users can customize the strategy's calculations with the following additional inputs in the "Settings/Inputs" tab:

Start date : Sets the date and time when the strategy begins simulating trades. The script marks the specified point on the chart with a gray vertical line. The plots for rules 2 and 3 display the bands and trading zones from this point onward.

Period : Specifies the number of bars in the linear regression channel calculation. The default is 40.

Linreg source : Specifies the source series from which to calculate the linear regression values. The default is "close".

Range source : Specifies whether the script uses the distances from the linear regression line to closing prices or high and low prices to determine the channel's upper and lower ranges for rules 2 and 3. The default is "close".

Zone % : The percentage of the channel's overall range to use for trading zones with rule 3. The default is 20, meaning the width of the upper and lower zones is 20% of the range.

SL% : If the checkbox is selected, the strategy adds a stop-loss to each trade at the specified percentage distance away from the closing price where the entry order occurs. The checkbox is deselected by default, and the default percentage value is 5.